The post Unlocking the potential of digital analytics in finance and banking appeared first on Piwik PRO.

]]>SUMMARY

- Financial organizations must optimize the digital experiences they offer to meet evolving customer expectations, focusing on user-friendly features and responsive customer service to reduce churn and improve retention.

- The implementation of web analytics presents challenges for financial institutions, as they need to consider aspects like regulatory compliance, data security, and the integration of disparate data sources.

- By leveraging analytics, banks can personalize customer experiences, optimize marketing campaigns, and refine product offerings based on real-time data and customer behavior analysis.

- Selecting an analytics platform that offers real-time insights, cross-platform analytics, high-level privacy and security features, and access to reliable data is essential for financial institutions to maintain competitiveness and ensure compliance with privacy regulations.

Many financial organizations do a great job gathering customer data. But to stand out, they need to anticipate customer expectations better and quickly adapt products and services to changing preferences.

Banks must ensure that their digital platforms are user-friendly, offering features like easy account management, instant transactions, integrated banking services in mobile apps, responsive customer service through chatbots or other digital tools, and more. Enhancing the overall digital experience can significantly reduce the likelihood of customers switching to competitors.

Strategically applying analytics is what banks are struggling with today. With this come the challenges of efficiently meeting customer needs, managing compliance, mitigating security risks and effectively applying analytics insights in different areas of business.

In this article, we will explore the challenges financial organizations face in analytics, how they can address them, and ideas for effectively applying analytics in their business.

Challenges of using analytics by financial organizations

Organizations in the finance sector handle large volumes of sensitive data spread across different systems and tools. This generates unique challenges for these organizations in implementing web analytics.

Regulatory compliance

Financial institutions must navigate a complex landscape of regulations, including data privacy laws such as GDPR. These regulations impose strict requirements on collecting, storing, and processing data. Non-compliance can lead to severe penalties, making it crucial for organizations to ensure that their web analytics tools adhere to these standards.

Data security and privacy

Given the high stakes involved in handling sensitive customer information, financial organizations are particularly vulnerable to data breaches. Third-party web analytics solutions can increase this risk, especially if sensitive data is stored on external servers. Organizations in the finance industry must choose analytics vendors that prioritize data privacy and employ the highest security standards.

Integrating data from disparate sources

Finance teams need to build a unified data system to effectively collect and store massive amounts of data from their own systems, different departments, and external sources. Many of these organizations struggle with data silos, where information is controlled by one department and isolated from the others. Data is often trapped in legacy systems that do not integrate well with modern analytics tools. This fragmentation makes it challenging to obtain a comprehensive view of customer behavior and limits the effectiveness of analytics.

Data quality

The effectiveness of web analytics relies heavily on the quality of the data collected. The sheer volume of data financial institutions collect can complicate reporting and analysis, requiring robust data management systems to ensure accuracy and relevance. Access to inaccurate data hampers the ability to effectively use analytics insights in marketing, sales or product development. Low-quality or inconsistent analytics data poses significant challenges for financial organizations, affecting their operational efficiency, decision-making processes, and overall trustworthiness.

Experts opinion

Jarek Miazga

Product Manager at Piwik PRO

Financial institutions are struggling to create comprehensive customer journeys because of insufficient data tracking capabilities in post-login areas. Additionally, they must carefully develop data-tracking strategies to comply with stringent regulatory requirements. This is just the tip of the iceberg, as they face numerous other challenges that demand attention and innovation.

Privacy compliance in finance

The finance industry deals with extremely sensitive data, often including personally identifiable information (PII). Examples include collecting visitors’ details such as names, dates of birth, home addresses, email addresses, demographic information, browsing history, device IDs, IP addresses, and more.

On top of that, they handle personal financial information (PFI), which includes account passwords, tax information, credit reports, credit card security numbers, and a lot more. Handling such information requires extra caution as any breaches can be particularly dangerous, leading to potential regulatory fines and loss of trust.

Financial institutions must comply with a large number of regulatory regimes and laws, which include strict sector-related restrictions, such as:

- The Gramm-Leach-Bliley Act (GLBA),

- The Dodd-Frank Wall Street Reform and Consumer Protection Act,

- The GLBA Safeguards Rule,

- The Sarbanes-Oxley Act (SOX), and many more.

At the same time, because financial organizations typically handle personal data and/or PII, they may fall under privacy laws governing these types of information, such as GDPR, CCPA, LGPD, DORA, and other global or local data protection regimes.

To align with regulatory requirements and ensure data privacy, financial organizations can employ the following strategies:

- Understand what privacy regulations they must adhere to and continuously monitor their compliance.

- Choose secure data hosting (e.g., in a dedicated database) in the location of their choice. For example, select an EU-based hosting provider if the institution is located in the EU.

- Maintain full ownership of data, how it’s used and what third parties it is shared with.

- Integrate analytics with a consent management platform to obtain valid user consent before collecting personal data.

- Communicate data collection practices to users through updated privacy policies.

- Apply data minimization to only collect the necessary data for specific purposes.

- Choose a privacy-conscious analytics provider that follows the privacy by design and privacy by default standards.

- Ensure their analytics vendor offers robust security features, such as SSL encryption, SSO authorization, access control, and data backups.

Practical use cases for web analytics in finance

Financial institutions can leverage web analytics to gain deeper insights into customer preferences. By understanding how customers behave across different channels, they can offer personalized financial advice, proactive product recommendations, faster response times, and customized alerts.

Let’s dive into the most important ways a financial company can practically apply analytics insights to their organization’s operations.

Personalizing customer experiences

Web analytics helps financial institutions track user interactions on their websites or apps, offering valuable insights into their engagement and interests. For example, they can understand how users navigate the website or app, their actions, and whether they complete funnels for specific goals, such as submitting a loan application or filling out a contact form.

By integrating analytics with a customer data platform (CDP), organizations can segment customers based on demographics, products or services they purchased, and website or app interactions. This segmentation enables banks to deliver personalized marketing messages and tailored content that resonates with specific customers, enhancing their experiences.

Find out about other practical applications of CDP: 8 customer data platform (CDP) use cases that will drive your business growth.

Improving marketing campaigns

Organizations in the financial sector can effectively use analytics data to improve their marketing campaigns.

They can measure and track their performance to refine and improve marketing assets and messaging in future campaigns. For example, they can analyze which channels drive the most traffic and engagement, recognize their audiences, and determine the best launch time for increased effectiveness.

They can also monitor content-related trends based on visitor activity and conversions, using these insights to influence their future content plans. For example, they can analyze page views, clicks, time spent on page, or file downloads.

Optimizing customer journeys

Web analytics also allows companies to identify pain points within the customer journey. With customizable reporting features, financial institutions can track how users navigate their websites or apps and analyze whether they complete the desired journeys.

One approach focuses on the small steps that users take that make up whole customer journeys, including:

- Evaluating available account options.

- Opening a bank account and onboarding.

- Making money transfers.

- Checking the account balance.

By identifying friction points for customers and where they drop off, organizations can address users’ issues and understand which interactions drive users to convert into paying customers. This can ultimately lead to a smoother user experience, increased customer satisfaction, and better business outcomes.

Reducing churn

Understanding customer behavior through analytics helps financial institutions predict and prevent churn. Financial organizations can establish feedback collection across channels – such as through surveys or social media – to understand the issues behind churn.

They can spot other signs of dissatisfaction, such as reduced engagement, to proactively reach at-risk customers with personalized retention strategies, including tailored products, incentives, or dedicated support. Additionally, they can regularly monitor KPIs such as customer lifetime value (CLV), churn rates, and satisfaction scores to measure the effectiveness of their retention strategies.

Developing products and services

Analytics insights are essential for continuous product optimization. By tracking metrics such as page views, clicks, conversion rate, or bounce rate, financial institutions can evaluate the performance of product pages and see how well their offers respond to prospects’ needs. They can also regularly analyze customer feedback gathered through surveys to refine their offer and adapt to customer expectations, ensuring their competitive edge.

Predicting trends

With analytics, financial organizations can assess historical data to predict future trends. For example, they can use available data to identify potential customers’ interests, target them with relevant offers at the right time, and optimize cross- and upselling opportunities. They can also make informed decisions regarding loan approvals and customer segmentation by assessing the risk levels using existing data.

Learn more about the benefits of analytics for financial institutions: BOŚ optimizes its business, product and marketing strategies with insights gathered through Piwik PRO.

Experts opinion

Carmen Jiang

Senior Digital Analyst at Vekst

An organizational and technical routine is crucial for organizations within banking and finance to set their digital analytics for success. Such routine should systematically encourage cross-department collaboration in both implementation, documentation and periodical review of its data collection. Digital analytics needs allies to foster a strong foundation within an organization, so don’t do this alone, and be vigilant and proactive in all your practices.

Key features of an analytics platform for finance and banking

When selecting an analytics platform, financial institutions should prioritize several key features to gain access to accurate, integrated data that they can effectively apply to their marketing or sales operations.

Access to actionable data

Web analytics should provide actionable insights to drive marketing strategies and improve user experiences. Companies need accurate, unsampled data to better understand customer behavior, optimize marketing efforts, and enhance the customer journey. Features like A/B testing, heatmaps, and customer journey mapping can help in identifying strengths and weaknesses in user interactions.

By combining analytics with customer data platforms (CDPs), organizations can apply the collected insights to create targeted marketing campaigns, provide tailored offers or send personalized emails.

Learn more about CDP benefits: Customer Data Platform: Generate meaningful insights with customer data activation and import.

Real-time data insights

Real-time data analytics is crucial for timely decision-making, risk management and operational efficiency. It shows how many people are interacting with a website or app, and what goals they are converting.

Financial institutions can use this data to dynamically manage their marketing content and campaigns. On the other hand, they’re able to monitor transactions and identify anomalies to detect fraudulent activities as they occur. They can customize real-time dashboards to visualize the most critical data and simplify day-to-day data management.

Learn more about real-time analytics in Piwik PRO: Real-time reporting: The complete guide.

Integration between systems and data

Integrating customer data across different systems and tools is essential for smooth data flow. It also provides access to unified first-party data sets that can be effectively used by other departments, be it marketing, sales or customer service. Working on consistent data reduces the risk of errors and helps enhance the effectiveness of data processes.

Financial institutions should opt for analytics platforms that offer seamless integration with other tools in their data ecosystems. They can also connect a customer data platform (CDP to integrate data from multiple sources, segment customers based on behavioral or demographic attributes, and activate data to target audiences with relevant marketing campaigns or personalized offers.

Cross-platform analytics

Cross-platform analytics provide insights from different platforms, helping financial institutions create funnels to identify and track users between native mobile app, WebView and website. This is especially vital for banking, where customers have grown accustomed to an omnichannel experience.

Reliable data

Financial organizations need to use an analytics platform that gives them access to accurate data. Analytics vendors often use data sampling, which only shows a subset of data. While sampling may be helpful in certain situations, it can lead to far less accurate reports and hide crucial insights, directly impacting business efficiency. Additionally, financial institutions can benefit from access to raw data, which gives analysts more possibilities for in-depth analysis, exploring data insights and making them actionable.

Dedicated support

Reliable support services from the analytics provider can significantly improve the platform’s effectiveness. Institutions should look for vendors that offer dedicated support services rather than relying solely on automated systems or chatbots. For complex data setups, companies may benefit from access to technical support in implementing their analytics infrastructure.

Conclusion

As the financial landscape continues to shift, having access to actionable insights will be crucial for maintaining competitiveness and fostering customer loyalty.

By choosing an analytics vendor that prioritizes privacy compliance, data security and access to valuable, actionable data insights, financial organizations can improve their marketing strategies, enhance user experiences, and ultimately drive better business outcomes.

Reach out to us to discover the full potential of Piwik PRO as an integrated analytics platform that satisfies the needs of financial organizations:

The post Unlocking the potential of digital analytics in finance and banking appeared first on Piwik PRO.

]]>The post How web and product analytics improve the customer journey in banking (while also maintaining security and privacy) appeared first on Piwik PRO.

]]>The answer is to collect data in the right way while actively minimizing and managing those risks. That’s what we’ll show in this whitepaper. We’ll also give you some actionable steps you need to take to enhance the digital journey for your customers.

What challenges do banks face in improving the customer journey? And how can they tackle them?

Security – Security of information is integral to banks’ operations as they handle consumers’ personal data, which is often of a sensitive nature. Appropriate safeguards mean you control where data is kept and who has access to it, so you’ll be able to minimize the risk of data leaks and breaches as well as prevent malicious attacks.

Data residency – If your bank has an international presence, you need to be aware of the local data privacy laws of countries you operate in. Some countries require storage of their residents’ personal data within the nation’s physical borders. To meet those obligations you need to choose a proper hosting option that allows you to keep the data in a compliant location.

Data transfers restrictions – Transferring data, especially personal data, is a tricky business. Regulatory issues of many kinds limit where you can send data. The solutions differ based on where you operate, but there is one constant: you need to remain in full control of your data. This means knowing what kinds of data you collect, where it’s stored and when it’s transferred. It also means having direct influence over all three.

Industry restrictions and internal protocols – Banks face a challenge of compliance with numerous regulatory frameworks, laws, sectoral restrictions and internal protocols. Unfortunately, there’s no one-size-fits-all solution. Some apply globally, others vary from country to country or between businesses. The key is the awareness of those that impact your business, then following them.

Reliance on third-party data in your advertising strategy – Financial institutions that carry out advertising campaigns tend to rely on third-party audiences bought from other businesses. But this approach is becoming problematic considering that the availability of third-party cookies is decreasing, and the quality of that data is low. Still, you can do successful marketing using first-party data.

The lack of a unified view on the customer journey and ad spends – If you run web or app analytics projects within your organization, you may find it hard to measure the value of your investment. That’s because data is scattered across different tools and systems. The solution is to have one platform that enables you to collect, stitch and use that data.

Improving the customer journey in banking

If you’re setting up to optimize your customers’ journey in your bank, your first step is to get the complete view of your customers and the path they follow with your organization. That requires data and the right piece of software that lets you transform it into action.

Once you overcome the challenges we’ve mentioned, you’ll be able to focus on improving the user journey. This involves removing bottlenecks, awareness of the micro journeys you need to take care of, and finally encouraging customers to engage with your products more.

Download our white paper to get more details on the challenges we’ve discussed and how to apply the solutions. You’ll also find an overview of how to optimize the customer journey and practical use cases, such as:

- Use case #1 How to optimize onboarding and improve engagement

- Use case #2 How to increase the number of credit applications

EBook

How web and product analytics improve the customer journey in banking (while also maintaining security and privacy)

Everything from security safeguards, compliance with privacy-regulations, data transfer restrictions and practical use cases

The post How web and product analytics improve the customer journey in banking (while also maintaining security and privacy) appeared first on Piwik PRO.

]]>The post How to run web & app analytics projects across banking groups appeared first on Piwik PRO.

]]>The problem is even greater for institutions with a worldwide presence. Because of strict privacy and security regulations – both sectoral and regional – they prefer to operate on the least amount of information about clients and support their advertising campaigns with data bought from third parties. But the new restrictions on third-party cookies introduced by Safari, Firefox and Google Chrome browsers are making this plan barely feasible.

Fortunately, there are other options that revolve around using a bank’s first-party data instead.

In this article, we’ll show you how multinational banking groups can track user behavior across applications and websites, and leverage this data in promotional campaigns effectively, without breaking laws or disrespecting users’ privacy.

The challenge of tracking ad spends and user behavior in banking

According to the Guardian, by 2021 the number of customers communicating with banks using apps will overtake that of the customers visiting physical bank branches.

This means that if you’re responsible for executing web or app analytics projects, you may feel that the stakes are getting higher and higher.

To make things work, you need detailed audiences to target with relevant ads and offers. Then, you need to know how new clients use your products and adapt to them.

Typically, such an undertaking involves stakeholders from across the entire group – different business lines and regions – that report directly to you. To make sense of all the data coming your way, you could create a “master view” of all the marketing collateral, such as:

- Number of downloads

- Ad spends and effectiveness of ad campaigns

- User behavior inside web or mobile application

- NPS/Apple Store/Google Play ratings

However, the following problems may occur:

1) You use multiple ad platforms

In many cases, teams across countries and business lines use different advertising channels and tools. Because of that, you may struggle when trying to compare ad spends and conversion rates across regions.

2) You don’t have a unified view on user behavior on the website or inside the app

Another thing is that there are often different owners of marketing and post-login pages or apps. People in charge of landing and marketing pages usually work with a corporate subscription of Google Analytics 360. However, the Mountain View giant’s software for many reasons is not a good fit for pages and apps accessible after logging in, also known as secure member areas.

A recent report by Brave explains in great detail the dangers of employing Google Analytics on websites containing confidential information about users. Be sure to check it out.

Keeping the data from those areas of websites and apps in a private cloud or with a trustworthy vendor is a much safer option. This is why, to mitigate the risks involved in using Google, teams responsible for post-login pages and apps tend to:

- use Adobe Analytics or a combination of Adobe Analytics and SiteCore

- fetch the data from server logs – this way they don’t have to apply tracking codes in sensitive areas of their portals

- build their own products to avoid involving any third party in the process

This number of analytics tools accumulated in your organization not only makes the costs of licensing/development and maintenance skyrocket. It also makes it hard or even impossible to connect the dots between individual steps in the user journey.

As a result, you can’t see things like which marketing websites customers had visited before they decided to open another savings account or apply for a mortgage. Also, you don’t know their previous steps, such as which advertising campaigns have brought the customers with the highest account balance.

COMPARISON

The comparison of 10 web and app analytics platforms

Learn the key differences between Piwik PRO Enterprise, Google Analytics 4, Matomo Cloud, Adobe Analytics, AT Internet, Countly Enterprise, Mixpanel Enterprise, Amplitude Enterprise, Snowplow Enterprise, and Heap Premier.

3) You need to respect data residency & privacy laws

Apart from that, you have data residency and privacy laws to abide by.

Numerous countries, such as Germany, Australia, Canada, India, Switzerland, Russia and China have introduced laws that order companies to keep their residents’ personal data within a country’s physical borders.

Storing data is one thing, but there are also data transfer rules you need to observe. For instance, GDPR allows it only if an adequate level of security is met. Transferring personal data is possible within the Privacy Shield framework, but you need to ensure that your organization’s compliance team reviews it case by case.

Update: As of July 16th 2020, Privacy Shield is no longer a valid legal framework for transferring data from the EU and Switzerland to the US. The situation is evolving fast, though. Here we’ve written about the decision and will provide updates when anything changes. And here we’ve written about how such limitations affect users of Google Analytics.

Also, there are many other privacy laws – such as Brazil’s LGPD, California’s CCPA, India’s Personal Data Protection Bill, just to name a few – with their own restrictions regarding data transfer. You can read more about them here.

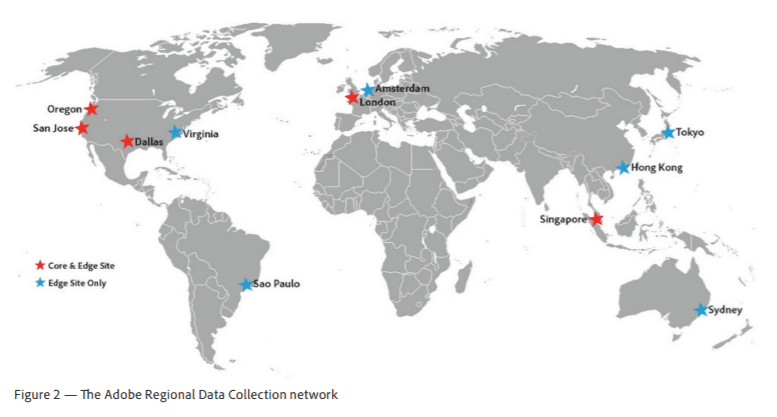

Meeting all those requirements is particularly difficult if you use Google Analytics and/or Adobe Analytics. None of them provides flexibility in terms of server locations. For instance, Adobe Analytics servers are based in the following regions:

With Google Analytics 360 you get no choice and the data will be allocated across different Google Data Centers. Here you can find their whole list.

To steer clear of violating data residency and privacy laws, your teams may decide to operate on the least amount of information possible, and what’s more – avoid collecting personal data at all cost. This means that, for example:

- they don’t feed their datasets with financial, CRM, offline or transactional data

- they’re unable to differentiate traffic between customers and first-time visitors

Consequently, the information your organization gathers is not only anonymized but also trapped in the silos of departments.

4) You need to stop relying on third-party data in your advertising strategy

Because of the problems with in-house data, you probably invest significant sums in the third-party audiences bought from data management platforms (DMPs), such as Lotame, Nielsen, The Trade Desk or BlueKai and push them into ad networks. Unfortunately, that is about to change.

Safari and Firefox’s new privacy features have reduced the availability of third-party cookies by around 30% to 40%. Now, Google has announced that it will stop supporting third-party cookies by 2022. Because of Chrome’s worldwide popularity, its new policy will bring the figure close to 100%.

This means that in less than two years you’ll have to learn to live without:

Buying audiences based on third-party data: The change will affect most of the DMPs that sell third-party audiences or map offline data to online identifiers on the web.

Data activation on the web: Using cookie syncing to identify and target users (e.g. by exporting an audience to a DSP for media buying).

Retargeting on the web: Showing ads to users across the web who have previously visited your website.

Attribution: Attributing ad views to conversions.

As a result, although ad networks will still be able to display ads on websites, things like behavioral targeting, attribution, and reach will become extremely ineffective.

- What Intelligent Tracking Prevention (ITP) Means for Web Analytics & Marketing

- Google Chrome Will Wipe out Third-Party Cookies. What’s Next?

- Google Chrome To Kill Off Third-Party Cookies: What It Means for AdTech

- Google Chrome’s Impact on AdTech & MarTech

- Privacy in AdTech FAQ: Google Chrome’s Privacy Sandbox, Safari ITP, Firefox, GDPR

First-party data comes to the rescue

In this situation, as a person responsible for a web or app analytics project, you may feel trapped because:

- You have to operate on fragmentary and anonymous information on the usage of your products, which is extremely difficult to combine into one whole.

- You’re unable to attribute monetary value to conversions on your websites or inside your apps.

- The sources of third-party data are slowly drying up and your internal databases are too scarce to create meaningful advertising audiences out of them.

Fortunately, there is a way – unlocking the potential of first-party data. However, in this case anonymous information is not enough to build the full picture. For this, you’ll need customers’ personal data. This means that you’ll have to opt out of Google Analytics and Adobe Analytics, since the platforms don’t really welcome this kind of information.

The Google Analytics privacy policy says this:

To protect user privacy, Google policies mandate that no data be passed to Google that Google could use or recognize as personally identifiable information (PII).

This, in turn, is how Adobe Analytics addresses the issue:

Adobe strongly suggests customers refrain from passing personally identifiable information (PII) to Adobe, especially in situations where the PII is not necessary for analytics.

To avoid violating products’ terms of service, you may want to consider different options available on the market.

The Piwik PRO Analytics Suite – consisting of Analytics, Tag Manager, Consent Manager and Customer Data Platform – allows you to achieve even better results without increasing costs, breaking laws or reducing your marketing effectiveness.

Because Piwik PRO is available in private cloud and cloud hosting options, you’ll be able to take advantage of the following setups:

- Private cloud deployment in each country with strict data residency laws – used exclusively by a certain region or department:

- A private cloud (dedicated hardware) keeps all server resources and databases storing analytics data physically separated and dedicated to one organization.

- A private cloud (dedicated database) shares server resources between customers but keeps them logically separated. Databases storing analytics data are physically separated.

- Bring Your Own Key encryption on private cloud (dedicated hardware) on Azure. This solution allows for the encryption of analytical data using the customer’s key but applies only to solutions hosted on Azure.

- Cloud deployment can be used in every country where no sensitive or personal information is being processed.

- A separate instance for an “executive view” with its own tracking code on instances 1) and 2) and a metasite for measuring high-level traffic across every area of your operations.

By using private cloud only where it’s necessary, you’ll also optimize infrastructure costs.

That will allow you to:

1) Gain an overview of the marketing performance of your project

Although in your “executive view” you won’t see all the details, you will be able to follow the progress of work and measure the performance of different regions and business lines in one place. This will allow you to make faster and more informed decisions.

2) Respect the laws and collect personal data

The locations of your Piwik PRO instances will be consistent with residency laws. What’s more, the data, except for high-level anonymized information, won’t be sent outside the borders of a given country or accessed by any third party.

As for data privacy regulations – Piwik PRO Consent Manager will help you obtain visitors’ consents as required by GDPR and LGPD. By using it, you’ll also be able to collect and process user requests resulting from the mentioned rights as well as legislation such as CCPA.

Here you can read more about how Piwik PRO Consent Manager can help you act in line with privacy laws around the world.

3) Capture the full customer journey

With the platform, you’ll be able to map the customer journey across different channels and follow user flow without missing any significant data points. A Customer Data Platform will allow you to integrate data from such systems as:

- CRM, marketing automation software

- Ad platforms

- Banking transactional systems

- Lead capture forms

- Social media platforms

- Other systems via API or through CSV imports

Visit this post for more tips on how to leverage sensitive and personal information in your marketing strategy: 4 Burning Questions about Onboarding Personal Data and Personally Identifiable Information (PII) to Your Analytics Platform

Thanks to this, your teams in each region will gain a well-rounded view of user behavior and attributes from all relevant sources, not just websites or apps.

Psst! With this kind of data at your fingertips, you’ll also be able to employ advanced customer retention strategies. Read more about that here:

However important it is to get a thorough understanding of your customers, getting the complete picture of their journey should never come at the expense of privacy and security. Also, you should consider implementing some extra security measures such as single sign-on, encryption, or a change log to make sure the data is safe and sound.

For more information on how to map the full customer journey in banking, check out this post: How Analytics & Customer Data Platform Can Help You Track the Full Customer Journey

4) Create a future-proof advertising & marketing strategy

Even though third-party data will no longer be relevant in the advertising context, there’s an opportunity to breathe new life into first-party data. In the eyes of marketers and advertisers, it’s considered an extremely valuable source because it’s collected from people who have a direct relationship with the brand: customers or potential customers who have had some interaction with it.

With Piwik PRO, you’ll be able to use your first-party data to:

Run on-site personalization & retargeting campaigns

With a wealth of customer data at your disposal, you can employ on-site personalization and retargeting. A combination of Piwik PRO Tag Manager, CDP and Analytics, will allow you to:

- Identify existing clients and target your audiences better (e.g. you won’t advertise opening an account to someone who already has one, you won’t show a loan offer to somebody with a low credit score).

- Build precise audiences based on different conditions, e.g. actions users perform on transactional pages, offers they’ve seen or the usage of the given functionality.

Thanks to the safeguards we discussed earlier, you’ll run your campaigns both on marketing and post-login pages without violating visitors’ privacy.

For more inspirations on leveraging on-site personalization and retargeting in your marketing strategy, visit these posts:

Gain a better view of ad spends and conversion rates on your websites and in your apps

The platform also helps you gain a better view of your advertising expenses:

- Your dataset consists of information about user behavior from many touchpoints, including ad platforms, marketing websites and secure member areas, among others. This, in turn, will let you e.g. calculate the proper cost of customer acquisition per channel.

- By setting up and measuring similar goals across every website (e.g. your national websites in US and Canada or Germany and Switzerland), mapping them and attributing a monetary value to each goal conversion, you can monitor the performance of your ad campaigns. You’ll know what works and where to funnel a bigger budget next time around.

These are just ideas for leveraging the first-party data collected with Piwik PRO. It’s worth keeping your finger on the pulse of how the AdTech market adapts to the recent changes. Our friends from Clearcode predict that the industry will start offering more opportunities for using first-party data and sharing it with trusted advertisers. To stay up to date, follow their blog.

If you want to read more about the benefits of using first-party data, here you go:

5) Save time and money

And let’s not forget about reductions in costs. Using one analytics platform, you don’t need to spend your whole budget on multiple tools and licences, such as Google Analytics 360 or Adobe Marketing Cloud to do your tracking. Here you get an all-in-one platform to collect data from multiple sources and finally put it into action. That saves you both time and money.

Also, a leaner analytics stack also means fewer products for your security teams to vet.

Conclusion

The world of AdTech and MarTech is undergoing a rapid change. Fortunately, banking groups can prepare themselves for it by unlocking the power of first-party data. This will not only allow you to build precise audiences based on data about people with real relationships with the organization. It will also help you gain a full picture of user behavior at every stage of the user journey and better measure the costs of customer acquisition.

Such a change, however, requires a sensible approach to the data your visitors decide to share with you and adjusting your ways to the demands of regional and sectoral regulations. Part of the task will be to find business partners that ensure an appropriate level of data privacy and security.

If you would like to learn more about how Piwik PRO can help you collect customer data in a responsible way, be sure to contact us. Our team will be happy to answer all your questions.

The post How to run web & app analytics projects across banking groups appeared first on Piwik PRO.

]]>The post 7 Areas to Consider to Improve a Digital Bank Account Opening Process appeared first on Piwik PRO.

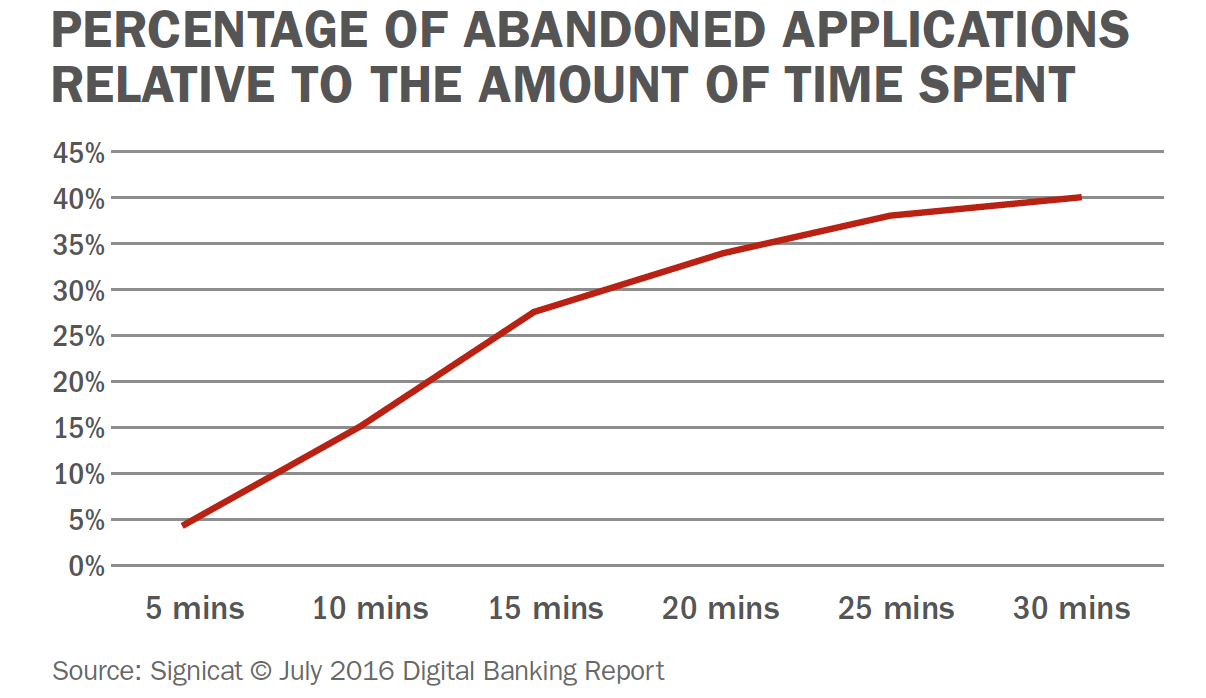

]]>Still, the abandonment rate for opening online accounts is 19%, as we learn from the Digital Banking Report. Another study, by Signicat, reveals that as many as 40% of online applications never get completed. So there’s obviously room for improvement and new opportunities. Most importantly, you need to grasp why so many people struggle to complete this task.

One of the biggest culprits is that the process is often confusing and requires a lot of work from customers. According to research by CEB (now Gartner), 96% of customers who put a considerable effort into an interaction become more disloyal. That’s why you need to ensure the procedure is smooth and simple from end to end, whether on a desktop or mobile.

For financial institutions, the challenge is even greater. People expect an experience as simple and pleasing as from apps like Uber or Airbnb. Above all, it needs to be fast and intuitive. The thing is, these applications don’t have to deal with the same legal and compliance issues as banks do.

But with the right technology, like analytics, and a sound strategy banks can streamline the process so people can open accounts with just a few clicks. Today we’ll present the key considerations that will help you reach this goal.

1. Legal and technical stumbling blocks to overcome

If you’re looking to optimize the procedure for opening a bank account, you need data. And there’s a wealth of it to be collected, since each step of the operation involves multiple forms containing personal and frequently sensitive data. This, in turn, entails an obligation to meet various regulations and have appropriate security measures in place.

Learn more about different kinds of data by checking out our posts:

From a technical standpoint, you need to be sure that your software provides your organization with the utmost security and full control over your data. As a bank, you operate within strict protocols and policies that specify who can access certain data you gather.

In that case, you can’t rely on solely cloud-based software like, for instance, Google Analytics. What’s more, not every vendor offers the highest standards of data protection.

The most airtight solution would be on-premises analytics that complies with stringent security and legal policies inside the bank. Self-hosting deployment allows you to supervise the application. That means you know where your data is sent – into your own servers, kept under your watchful eyes.

Also, you get full access control, so you’re in charge of your infrastructure configuration. You can tailor it according to your bank’s security rules.

If you want to compare different hosting options and see which one would best suit your needs, check out:

How to host your analytics: public cloud vs private cloud vs self-hosted

However, internal rules are just a part of the story. Besides internal regulations, you need to consider the legal landscape. With growing awareness of user privacy and data security issues, there’s more than just GDPR to think about. For example, there’s the California Consumer Privacy Act, Brazilian General Data Protection Law (LGPD), Chile Privacy Bill Initiative, and China Internet Security Law.

The good news is that if you have adopted a GDPR-aligned framework across your bank, then compliance with other laws will be much smoother. In some cases it might even mean you’ve done most of the heavy lifting already.

Dive deeper into privacy laws around the globe and check out our posts:

2. Defining business requirements

For banks, credit unions and other financial organizations, reducing frictions in the process entails designing a sound strategy. That involves specifying business requirements, determining what needs to be measured to optimize each step.

Start small and consider basic UX metrics that will give you the bigger picture, like:

- conversion rate

- process success rate

- abandonment rate at each step of the process

- the average time it takes to open an account

For instance, abandonment rates are most acute when people are going through online identity verification.

Once you grasp the state of affairs, you can dig deeper. After UX and analytics metrics, focus on business metrics. There are certain things you need to analyze. For example, think how each change to the process of opening an account impacts its quality. Or whether a drop in the number of accounts opened correlates with an increase in their business value.

To get a broader perspective on collecting business requirements, take a look at:

10 Steps to Gather Business Requirements for a Robust Web Analytics Strategy

3. Preparing an implementation plan

After you have requirements and goals in place, the next step is to convert them into an implementation plan. This is the ideal tool to ensure you’re tracking all key interactions during the account opening process. It also covers resources, budget, outcomes and responsibilities. Finally, it serves as a technical guide that turns business needs into tasks for developers and technical teams.

Such plan transforms goals and ideas into identifiable steps, ensures you keep a record of all your activities so you won’t miss anything that’s crucial for the success of your business initiative.

To learn more about analytics implementation, we recommend reading:

Analytics Implementation in 12 Steps: An Exhaustive Guide (Tracking Plan Included!)

4. Spotting the friction points

To improve the process of opening accounts, you need to find where and why people struggle with it, or even abandon their efforts. It’s best to reach for basic but fundamental reports that help you understand user flow. Go for funnel visualization reports.

Read up on user flow:

3 Reports for Optimizing User Flow on Your Website

First, you need to segment data in the report and then break it into smaller chunks. Then, start to measure conversion and abandonment rates for the whole process as well as for individual steps. This data shows you the process’s breaking point faster.

With a properly configured report and attached metrics, you’ve got a perfect set of KPIs to track the process. Also, you can monitor if your optimization strategy is moving you closer to your goals.

Funnel reporting lets you do a quick “technical analytics” and UX overview of the account opening process. The last piece of this puzzle is segmentation. You can divide your customers by:

- device type

- browser type

- device manufacturer

- screen resolutions

You can apply more segments, but this should be enough to uncover 80% of the most basic technical issues.

You should be looking for answers to questions like: which user segments have higher abandonment rates? Does it matter if they use Apple or Huawei? What is the difference in abandonment rates between desktop and mobile users? And so on.

What’s more, insights from technical analysis are great guidance for your QA team. For example, by comparing abandonment rates between MS Edge and Chrome, you can indicate where the QA team should look for tech issues and bugs.

Once you know whether a particular form or step is the culprit, you can dive deeper by applying more granular metrics. If your analysis reveals that a form is causing issues, then shift your focus there and analyze customers’ interactions field by field.

5. Looking for flaws in the account opening process

Before you move any further, determine whether a form is the troublemaker. Crunch the numbers – how many users have interacted with the form but eventually abandoned it, and how many of them didn’t even start. If either percentage is high, then it’s worth analyzing this customer segment separately.

For customer segments that didn’t even start filling out the form, check if the form displays properly. Another reason might be that it was way too long and complicated.

As for people who leave the form unfinished, you need to verify which exact field provokes them to drop it, and which other ones could be problematic later on. That calls for an advanced analysis.

To assist you in finding the culprit, here is a bunch of handy metrics from Formisimo, the industry leader in form analytics. Measure:

- How often people abandon or drop forms

- How many times people re-enter or correct field data

- Which fields are regularly ignored or left blank

- How many form submissions generate errors

- How long it takes to complete a form field (or the entire form)

Such metrics provide you with a complete picture of form issues. Once you identify the reasons why users are dropping out of the process, you can fix them on the spot and prevent further damage.

6. Time required for opening the account

The digitalization of banking services means that people expect to do business quickly and easily. The same goes for opening an account, and numerous surveys confirm that.

As found in the report titled State of the Digital Customer Journey, abandonment rates increase dramatically when the time to finish an application process increases.

Understanding this finding is crucial to optimize the whole process.

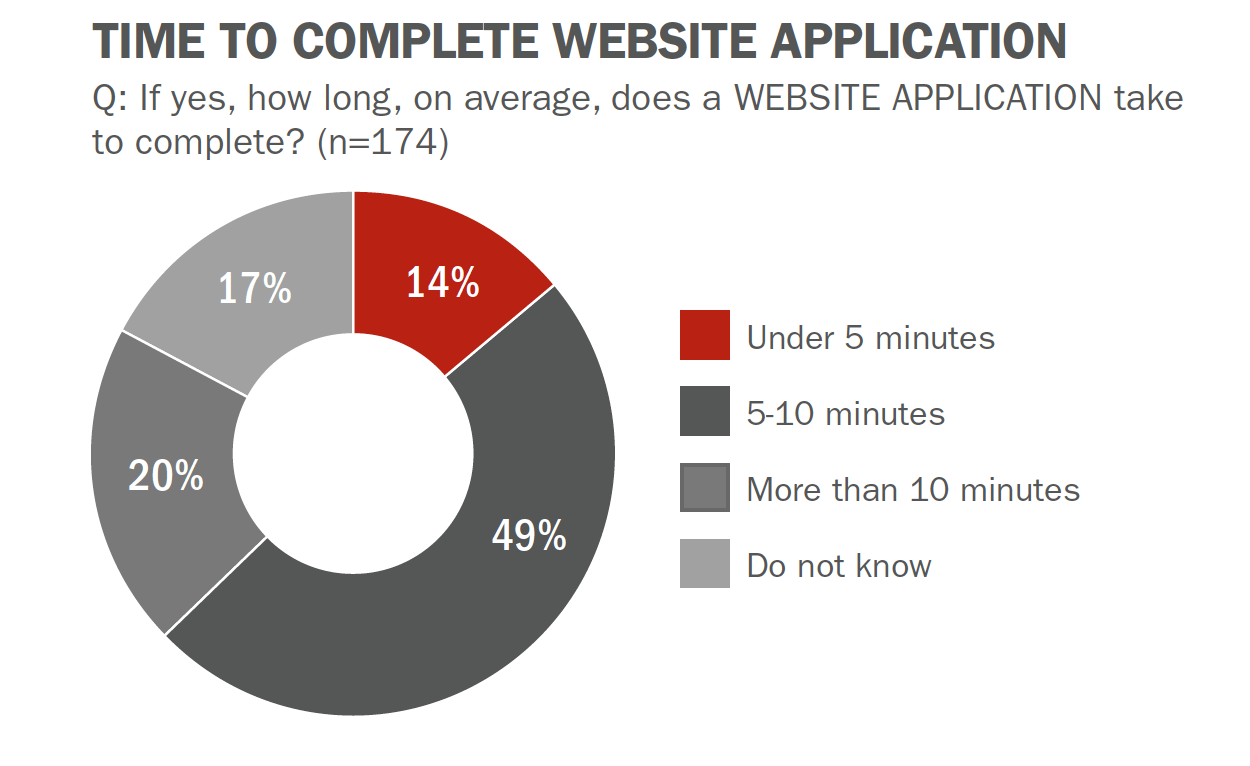

The numbers don’t lie. The Digital Banking Report reveals that barely 14% of organizations surveyed made it possible to finish the account opening process in not more than 5 minutes, while for 20% it takes over 10.

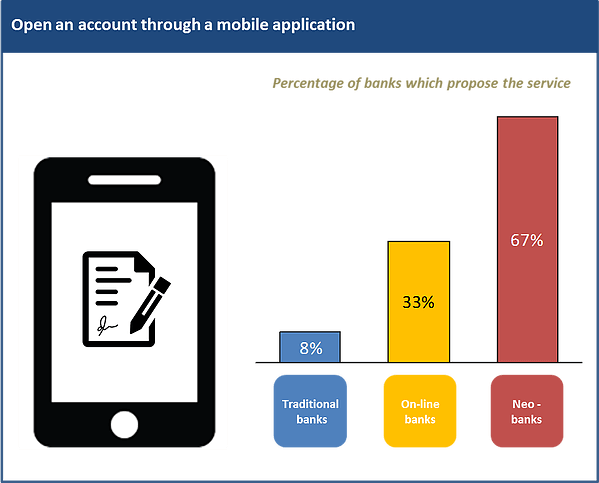

7. Optimizing opening a bank account for multiscreen experience

Mobile and online banking brings a host of challenges. The most critical of them is the account opening process – a dropped transaction can mean a customer is gone forever. Bad first experiences will destroy much of your efforts.

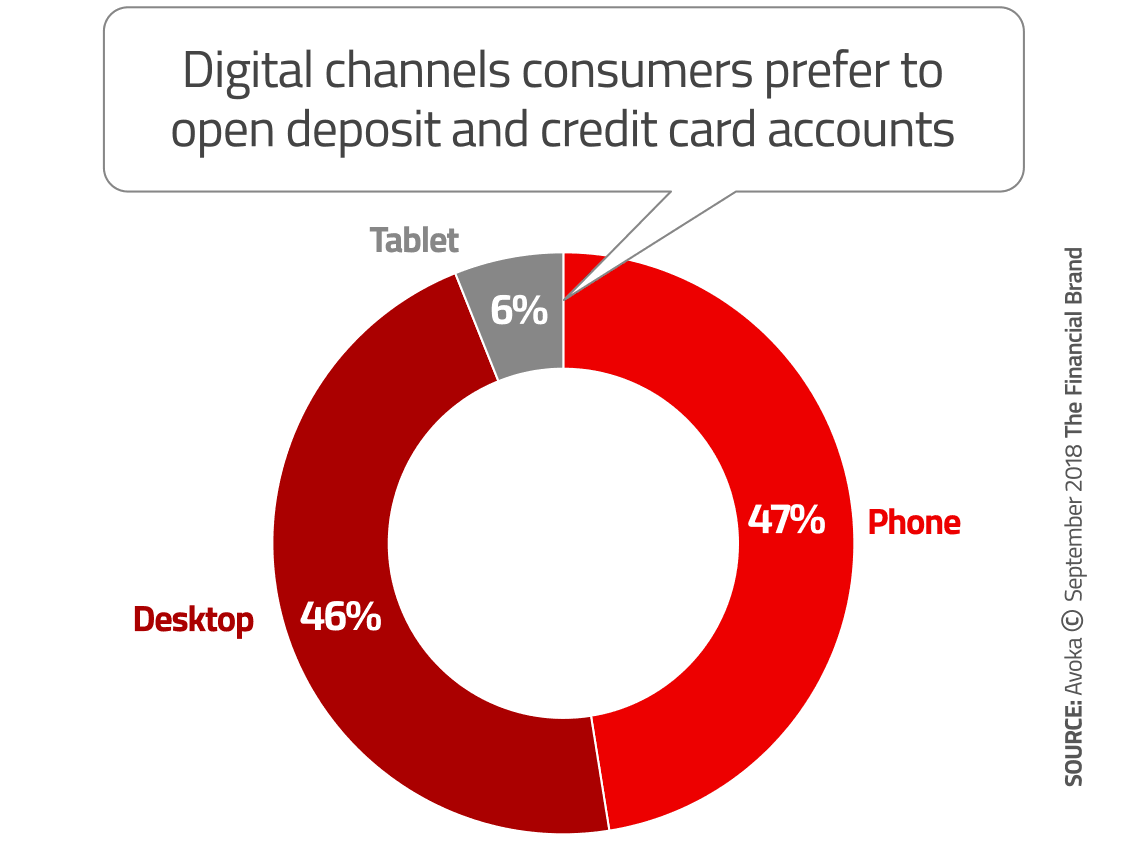

The problem is particularly acute for smartphones. Based on Avokas’s Digital Sales Report, more than 60% of digital applications in major national banks are sent via mobile phones. It means they have overtaken desktops. That’s why it’s essential to optimize the mobile experience when planning your acquisition strategy.

Moreover, streamlining the account opening process for mobiles is vital for Millennials, who top the mobile banking usage stats. They’re particularly demanding and show little patience for poor user experience.

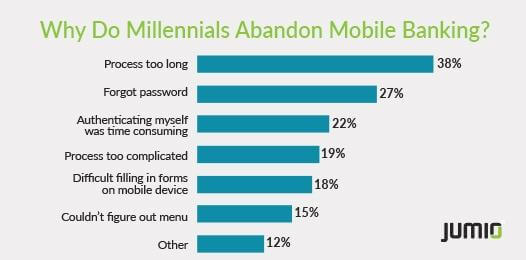

In truth, as found in a survey by Jumio, 38% of Millennials drop mobile banking activities when things take too long. It turns out that improving the process, cutting down on time and removing frictions is a competitive necessity banks need to focus on.

Best practices

Now that you know what you need to be looking for, it’s time for some actionable tips. To help you improve your overall strategy and save some time, we’ve gathered practical tips from the experts at The Financial Brand. Here we go:

- Simplify the form to the bare minimum. Make it fast and easy to complete. Ask only for the basic information that a person knows without checking any documents, like phone number or address. Any extra details you can gather later on. This helps you to reduce time, keystrokes and all unnecessary scrolling, which is a common issue on mobile devices.

- Make the process as digital as possible. Provide a way to submit documents via email or let users upload them online, support digital signatures so customers don’t need to visit a branch.

- Design with mobile in mind. A great experience on mobiles means a transaction is fast and doesn’t require much effort. Offer things like dropdown lists or toggle buttons so it’s easier for customers to supply information. Remember about reducing white space and including an adaptive design to ensure an excellent user experience across all kinds of mobile devices.

- Ensure “save and resume” functionality. While opening an account, customers often switch between channels so help them start the process and come back later without forcing them to take the same steps again.

- Retarget abandoned applications. People drop forms without completion for various reasons, be it low battery power, answering a call, or a lost internet connection. It’s crucial to obtain their primary contact information early in the process to retarget these applicants quickly.

- Postpone cross- and up-selling. First, focus on onboarding for the product your customer applied for. All marketing initiatives concerning additional services should wait until the account opening process is done.

- Ensure tool stability. Before you provide your prospects and customers with an app, make sure it’s free from glitches, bugs, etc. App failures and error notifications significantly impact user experience and unnecessarily extend the account opening process.

Final thoughts

Customers’ expectations are rising rapidly and a truly awesome digital experience across financial services is a must. That’s why long forms and complex account opening procedures need a serious makeover. Above all, banks and other financial players have to ensure the whole journey is 100% digital, and that it lasts much longer after clients activate their profile.

We hope that you will refer back to this article as you devise your optimization strategy. In case you want more details or have some questions about products you can use along the way, get in touch with us.

The post 7 Areas to Consider to Improve a Digital Bank Account Opening Process appeared first on Piwik PRO.

]]>The post 4 Ways Product Analytics Optimizes Onboarding in Online Banking appeared first on Piwik PRO.

]]>Based on research, financial organizations lose about $66 per year for every dormant account and only 45% of checking accounts generate reasonable revenue.

So, how can you ensure your customers actually use their account actively? By optimizing the onboarding process in online banking. In other words, helping your new customers get familiar with your product and engaging them more so they use it regularly. In order to achieve this you need to know how people interact with your product. This is where product analytics comes into play.

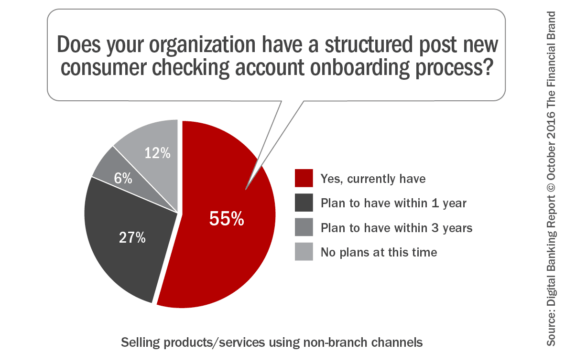

Also, as stated in Digital Banking Report, less than 50% of financial organizations have a structured onboarding process. Meaning there’s no outreach after a new account goes live.

Whether your organization faces a similar problem or just needs to see better results, we’re here to help you out. You’ll find some advice on how to optimize the banking onboarding process so your customers utilize your product more often and you get higher retention. These four points presented here are somewhat interrelated, but only some or all can apply depending on where you are in your digital transformation.

5 Major benefits of optimizing the onboarding process for online banking

Banks face numerous challenges in maintaining a strong market position. One of the ways to improve the situation is to make customers happy, address their needs at the right time, with the right offer. In other words, make sure you have an effective onboarding process of new customers in place. This will significantly enhance customer satisfaction and create a strong engagement strategy. But that’s just the beginning.

If you’re not sure whether you should devote additional time to improving the onboarding process, let’s look at some benefits in doing so:

- Improved customer loyalty: Successful onboarding processes propel customer satisfaction, retention, referrals and sales numbers. Onboarding is also presents a great opportunity for cross-selling.

- Higher retention and profitability: Ensure that the first impression with the account, a part of the onboarding package, is great. A great first impression will prompt new customers to use accounts more often and increase customer retention. Also, to have satisfied and engaged customers you need to keep an eye on some critical points to fix them on the spot. Customers who actively use your product have a significant impact on your organization’s profits.

- Enhanced operational efficiency: By introducing digital processes across all business areas you reduce manual work and increase accuracy.

- Better insights: The onboarding process is a great way to gather customer information from the branch as well as digital data before and after a purchase. All that, merged into a single record allows you to better understand your customers and their expectations.

- Risk mitigation: The sooner you create a 360-degree customer view during the onboarding process, the sooner you’ll have a high quality audit log of customer’s actions you can maintain. You can easily identify e.g. higher risk activities, and ensure compliance to the internal rules.

1. Convert business requirements into analytics KPIs

When optimizing the onboarding process a good place to start is by minimizing the time it takes to onboard a customer. The longer it takes to onboard a customer the higher the chances are of them looking for other options, outside of your bank. This is another challenge banks are facing. According to Digital Banking Report 2017 Account Opening and Onboarding, some banks are even losing 90% of customers with newly opened accounts.

That’s why your focus should be on improving user flow, clearing all the bumps in the road, and enhancing the UX of your online platform. To help you out a bit, here are the key KPIs you need to measure to make it all work:

- abandonment rate of the whole onboarding process

- success rate (conversion rate) of the whole onboarding process

- number of interactions needed to complete onboarding

- abandonment rate or exit rate on individual onboarding steps

However, as we already mentioned, getting a customer to open a new account is only the halfway point when it comes to success. To get from the halfway point to the finish line you need customers using your product frequently from day one and signing up for additional services like mobile banking.

But that’s not all. You want to become your customers’ primary financial institution, so they’ll perform all their transactions via your bank. Simply put, customers move their direct deposit account over from a different bank just as they’re getting a new account.

To assess engagement, you should pay attention to these KPIs:

- rate of new customer downloading & installing mobile application

- average daily or weekly number of logins into account

- average daily or weekly balance checks

- rate of new customers who move their deposit after opening an account

- adoption rate of debit cards

- adoption rate of features and products available for individual customer

- adoption rate of automatic transfers, alerts

- adoption of saving accounts and other available subaccounts

If want to find more information about KPIs for banks, but not only, have a look at:

2. Apply technology to refine the onboarding process

From a technical standpoint, tracking onboarding for online banking resembles product analytics since E-banking platforms are in fact a type of digital product with secure customer areas.

And as your starting point you should prepare a tracking plan. It gives you a wider perspective, ensuring you include all business requirements and that you set up your web analytics software correctly.

To get all the details on collecting and applying business requirements and tracking plans check out our posts:

So, let’s say you want to track engagement KPIs like adoption rate of functionalities and products available for an individual customer or rate of new customers who’ve set up direct deposit after opening an account. Then, you should use events, ones typically applied to tracking unconventional actions people perform with the product.

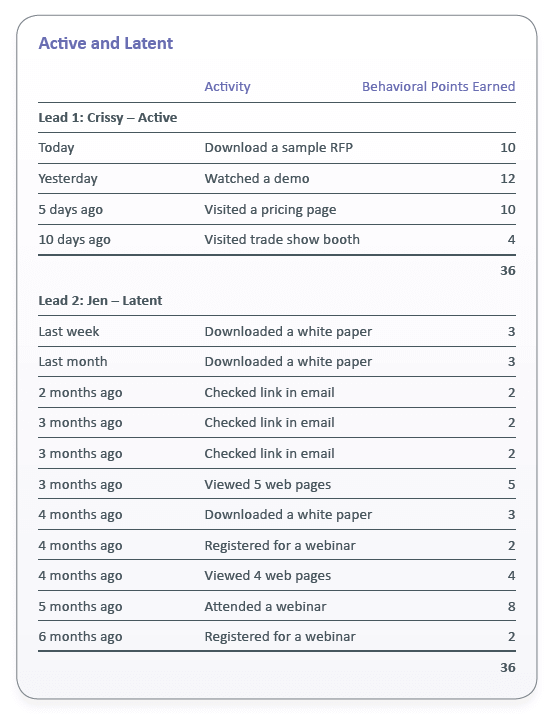

The metrics can be complex as customers engage with your product on different levels. If you want to track them and the adoption rate, you would need more than standard metrics and dimensions. Your ally for this task is scoring mechanisms provided by software like customer data platform (CDP).

But what exactly does it mean? So, scoring mechanisms attach a numerical score to every action and interaction the customer performs when they use the online banking platform. Then, the customer gets rewarded a number of score points for reaching every milestone in the onboarding flow. So they’re using new features and products, or finding new options with their new account.

This way you can define different score levels for different phases of the onboarding process. The customer who is halfway through the onboarding process should have between 20 and 30 points.

Thanks to scoring points, you can track the adoption of individual products and features available in the account. It enables you a detailed analysis helping to refine the platform’s UX.

Scoring mechanisms also help marketers and sales representatives to identify leads that are ready to move to sales and leads which require some more nurturing.

When you decide to apply this method of tracking user flow in the onboarding process you need to include assigned score points to individual interactions and events.

This is also a good moment to assess the value of particular interactions during the onboarding.

Think about customer engagement and which actions carry more weight when it comes to engagement. Is a customer more engaged when they set up automatic transfer or automatic alerts? Which of these actions should get more scoring points? We will cover how to use scoring points in detail a bit later.

COMPARISON

The comparison of 10 web and app analytics platforms

Learn the key differences between Piwik PRO Enterprise, Google Analytics 4, Matomo Cloud, Adobe Analytics, AT Internet, Countly Enterprise, Mixpanel Enterprise, Amplitude Enterprise, Snowplow Enterprise, and Heap Premier.

3. Create reports and visualizations of onboarding flow for banking

Onboarding is an intricate process. To improve its flow you need to visualize it. It helps you see the customer’s actions from different angles and with a wider perspective. Data itself won’t give you the whole picture, you need context.

Since it’s an ongoing process the experts from the Financial Brand recommend taking into account new households along with the current customers that sign up for a new account.

That is, you should perform onboarding processes for all types of accounts, deposits, loans, investment services, small business relationships. You can create them for other services like online banking, mobile banking, billpay, P2P transfers and mobile deposit.

In such a case, to make your visualizations clear and more efficient, you need to prepare an onboarding flow for every single product and every customer segment. You could, for instance, build a segment for enterprise, individual, small business, enterprises, investors, farmers, students and so on.

Ultimately, you need to create separate funnels and flow reports for every onboarding process.

Depending on what your organization offers, you could have onboarding flows for:

- new online account

- new credit card account,

- new saving account,

- other products like loan, mortgage, insurance etc.

Once you know what you would like to include in those flows, it’s time to dive a bit deeper. You can present them along with the onboarding processes by using classic funnel visualization reports, namely vertical or horizontal ones.

Keep in mind that each funnel report should allow you to segment customers. Otherwise the report won’t fulfill its full purpose and the data you get won’t tell you the whole story.

Simplify the banking onboarding process

As we’ve mentioned before, you need to reduce the onboarding time. One way to achieve this is by simplifying the whole process, helping customers to navigate more easily. Reduce unnecessary distractions and work on improving various functionalities.

But first, look at the way your customers interact with your site or mobile app. This lets you assess if different stages of that process are simple or rather difficult.

Also, take a closer look beyond the website or app interactions, Check what’s the abandonment rate on specific pages. Dig deeper and monitor the customers’ service calls, social media discussions and in-branch engagements to better understand the challenges that new clients may face.

If you’d like more details on reporting and visualizing customers flow in onboarding, check out:

4 Steps to Apply Product Analytics to Track User Onboarding

4. Optimize onboarding flow with the data you captured

If you’re seeking the main differentiator for large organizations, also financial ones, then it’s definitely customer experience. And that should be your focal point if you want to improve the way your banking customers get through the onboarding phase.

Start with basics, like checking the abandonment rates at different stages of the process. That should come really easily if you presented your onboarding flow using one of the funnel visualization methods.

When you find that at a certain stage a lot of users get stuck and leave, it means you need to do further analysis. Enrich your UX research with some extra data from mouse scroll and mouse click reports. You could employ for that job some additional tools or set up additional events dedicated to tracing mouse activity.

Then, you should find out which customer groups struggle during onboarding. Here, advanced segmentation capabilities of your reports come in handy. They let you closely watch particular customer segments and find roadblocks so you can fix them at once.

Also, while you work on improving the onboarding process you should consider the different levels of customers’ technical skillset. Maybe some of them would welcome extra assistance. Such information is crucial and can be reflected in scoring levels and created audiences in CDP. Then, your customer support team can reach out to clients, who got a lower score via call, email, livechat, and help them get through that phase more smoothly.

Find out why prospects turned into your customers

When you design an effective onboarding strategy, you need to know “why” your prospects became customers, recognize “Committed” (those who are 100% with your brand), from “Tire Kickers” (come for your offer, but rarely buys). If you need some guidance, then acquisition data should help you out.

- Offer – How diverse was your offer. Was it the motive to become a customer?

- Interaction history – How many times did you have to contact the prospect? Consider efficiency of different communication channels, and timing.

- Source – Did customer come through display or search ad, or direct marketing?

Such knowledge helps you more precisely segment your customers, address their needs more efficiently and better direct them to their goals across the onboarding.

Employ scoring points to measure customer’s level of interest

Thanks to tracking customers behaviors and applying scoring mechanisms you can measure how well customers know your product and how much it sparks their interest. With CDP you can build precise audiences based on the onboarding stages and implement various strategies to inspire users to become more active.

Because of that, you need to define scoring criteria. Let’s say, your prospect clicks a link in an email about a product discount. You should score it higher than one when they click on an industry link, because the product link implies buying intentions. That will also allow you to distinguish between active and latent buying behaviors and adjust your scoring.

That’s why your new customer starts their journey with 0 points as they haven’t used much of the banking platform. It’s a good time to send a trigger to your emailing platform and send onboarding welcome and educational emails.

In such manner you can show appreciation for choosing your bank and set customers on the right track to learn about platform’s benefits. Also, you can provide customers with an onboarding action plan that maps the timelines for messages and goals they will work towards.

The more that account holders interact with your banking platform and take advantage of its various functionalities, the more points you can grant them.

For instance, 10 for setting up automatic transfers and importing transfer recipients from the old bank account. As the score increases, you can move a customer to a new audience, like ‘Customers in the middle of the onboarding process’.

As customers switch their place across different audiences you can send them different messages, via pop-ups, banner notifications or emails, helping them find new, more complex possibilities of the platform. Finally, you can apply cross- and upselling campaigns, increase the adoption rate of other financial products available from the account level.

Conclusion

Because of the increasing expectations from customers and hardship to differentiate services, banks and other financial institutions need to improve their strategies to grow their base of loyal customers. With the help of technology like web analytics and CDP banks can offer a smooth onboarding process through removing all the obstacles, clearing the way to great customer satisfaction and increased retention.

We realize that this post might not address all the issues regarding such a complex strategy so if you’d like to get more questions answered, just reach out to us and we’ll be more than happy to help.

The post 4 Ways Product Analytics Optimizes Onboarding in Online Banking appeared first on Piwik PRO.

]]>The post Web Analytics For Banks: Off-The-Shelf vs. Build-Your-Own appeared first on Piwik PRO.

]]>With legal restrictions and internal policies, it’s much more difficult to take full advantage of the benefits that collecting data brings.

The marketing areas of websites and applications are usually analyzed with the use of common solutions like Google Analytics or Adobe Analytics.

The situation gets tougher when you collect data from the pages available after logging in, known as secure member areas. The data processed there often contains PFI (personal financial information), the use of which is regulated by a number of sectoral laws – including the MOBILE Act and PSD2 (Payment Services Directive 2).

According to SQN Banking Systems, the five biggest threats to a bank’s cyber security include:

- Unencrypted data

- Malware

- Non-secure third-party services

- Manipulated data

- Spoofing

This makes the use of popular tools with third-party scripts (like GA) extremely risky.

We’ve written more about it here:

How to Handle Marketing Data the Right Way in Banking Industry?

What makes this data useful? It’s where users perform the most important activities from the bank’s standpoint. This is where their true preferences show up. The data is ready to be pulled from transactional pages to allow banks to prepare better, more customized offers and increase customer satisfaction.

Combining data across marketing and secure areas of the website gives us the full customer journey.

There’s no need to give up on the idea of collecting this kind of data once and for all though. Here’s what you need to take into account when deciding on an analytics solution for banking:

- all of your sectoral limitations

- data security demands

- budget restraints

- what you want to achieve with the software

Read more about it here:

6 Problems to Solve When Choosing Web Analytics for Financial Services And Banking

There are at least several ways in which you can tackle the issue, including:

- building your own platform

- buying off the shelf analytics

Let’s take a closer look at these options and analyze their advantages and disadvantages.

1. Building your own software

This basically means that you use your own or outsourced workforce to code the solution from scratch.

You’ll get exactly what you asked for. This type of approach will require commitment on your part throughout the entire development of the product.

Let’s see the most popular ways of developing custom tools:

In-house development: pros and cons

The first and quite popular choice is to build a simple web analytics tool stored on your own premises. This tool will allow you to track users’ behavior, as it would be tailored to your specifications. As an alternative, you could take a pre-existing open source analytics tool (like Matomo or Open Web Analytics) and adapt it to your specific needs.

Possible pros

Accountability

The biggest advantage of this solution is that you’re working with a team employed directly by your company. Therefore, designers and developers involved in the project feel high responsibility for its success.

High adaptation to your needs

The tool will be a direct translation of your needs into an analytics system. It will be created based on your guidelines and business objectives.

High security

Going for your own tool means you can implement all the privacy settings necessary to comply with the relevant regulations. This is especially true if achieving full data privacy compliance is problematic when using an off-the-shelf tool.

Also, ownership of technology and data, rather than using a third-party solution, gives the advantage of intellectual rights ownership, better adaptability and compliance with privacy regulations.

Possible cons

Lack of analytics software development skills

Companies assume that the expertise of their own IT team will help them create software that fits their market.

After all, IT teams in banks have a high awareness of the banks’ limitations arising from laws and internal policies. However, fluency in web analytics software development is a completely different thing.

Keep in mind that developers must dedicate significant time to learning, creating and maintaining a technology. This technology is merely an addition to the bank’s core business. Unless your team has experience in custom analytics platforms, there’s a chance that the outcome of their work might be simplistic and limited. Integrations and user friendliness can be particularly problematic.

Continuous business engagement and commercial support

Another thing is the need for continuous business engagement and commercial support to avoid detachment. Building your own tool might seem like a project for the technologically savvy, but ongoing business engagement is of equal if not greater importance.

Cost

Acquiring the technology and expertise necessary to develop such a tool can be quite an expensive endeavour. Rolling out and developing a platform is one thing, but ongoing maintenance and operation also involves costs.

This can lead to a situation in which you will have to expand your IT team. And as you surely know, hiring developers directly is a lengthy and costly experience for any company. The average time it takes to recruit a new developer is 43 days, and involves extensive productivity losses.

You can reduce the cost and time of the exercise with the help of outsourcing. However, in this case, the expertise of the crew people and your impact on their work can be considerably lower.

Hiring a specialized software agency: pros and cons

A development partner is a company that specializes in a particular area of software development – in this case, web analytics. They typically provide full-service development as well as a dedicated team of specialists, including designers, project managers, DevOps, developers, QA and testing specialists.

One of the most popular software houses creating analytical systems is our sister company, Clearcode.

Quality

Because of specialization, the quality of the product is going to be a lot higher compared to the quality produced by inexperienced developers, regardless of whether they are in-house or outsourced.

What’s more, it can be designed to meet every requirement outlined in the evaluation phase. Rather than just labeling something ‘Nice to Have’, you can have it. Custom software can be modified and expanded, keeping in step with your business as technology and your business itself develops and changes over the years.

Technical resources

A development partner will have all the required resources needed to manage the entire technical side of the project. You can focus on building your business and onboarding new clients.

Possible cons

Cost

Like anything that is customized, a custom solution will cost much more than an off-the-shelf product. For companies operating on a limited marketing budget, the price may turn out to be an insurmountable obstacle.

2) Off-the-shelf web analytics

Another option is to use ready-made solutions. They will not be 100% tailored to your needs, but they will allow you to limit or completely free yourself from developing your tool in-house. Also, unlike custom platforms, they won’t require such a large up-front investment.

Here you’ll find the most popular solutions in that field:

Buying unintegrated systems: pros and cons

The first way is to buy non-integrated analytics modules. Such a hybrid system usually consists of:

- For marketing pages (e.g. landing pages, main website) – Google Analytics, Adobe or another popular tool using third-party scripts

- For secure member-only pages – a server log analytics tool, maintained on-premises

Instead of developing software on their own, banks can buy ready-made tools and develop integrations between them.

Possible pros

Cost

The cost of building such a system is much lower than developing software from scratch. Still, your internal team has to manage integration between the tools to connect the data. This means you have to bear some costs associated with internal development and maintenance.

Time

You’re able to put the solution to work almost immediately after you develop the integration between modules.

Possible cons

Quality

Integrating two solutions based on different technologies might be a challenge. Particularly if one of them collects data using javascript, and the other fetches the data from server logs.

Also, technical differences might cause a problem with unifying the data into a single structured set. Thus, the platform won’t deliver the high-quality data necessary to connect the dots across the stages of the customer journey.

Not to mention that using two different tools can lead to data discrepancies.

Buying off-the-shelf, integrated systems: pros and cons

Another option is ready-made analytics. You should look for web analytics vendors offering on-premises storage options and features for enhanced data security. Those might be difficult to find, since most analytics tools operate in a cloud environment. That automatically rules out running their software on a bank’s domain.

Piwik PRO Analytics Suite, however, unlike most of the web analytics tools available on the market, ticks all those boxes. Let’s see what you’ll be able to achieve with a product whose roadmap is shaped by the needs of the financial industry.

Possible pros

Time

By opting for ready-made solutions, you save time. The tool will be ready to use right after you install and configure it.

Cost